.png)

Why This Matters

Most business owners think about taxes once a year. In April, when it is already too late to do anything meaningful about them.

But the business owners who consistently keep more of what they earn? They think about taxes all year long, including summer.

Summer is actually one of the most tax rich seasons of the year. You are traveling for conferences. You are visiting properties. You are taking clients to dinner. You are attending networking events. And if you are doing all of this without a strategy, you are leaving real money on the table.

This post is for entrepreneurs, real estate investors, and high income business owners who want to understand how summer tax planning works and how to do it right.

Why Summer Is a Hidden Goldmine for Tax Planning

Business Does Not Stop and Neither Should Your Strategy

Summer tends to be a high activity season for many business owners. Industry conferences pick up. Real estate investors scout new markets. Client relationships get refreshed over meals and events. Deals get made on golf courses and at rooftop dinners.

The IRS recognizes that legitimate business expenses can happen anywhere, including on a trip that also has some personal time built in. The key is understanding what qualifies, what does not, and how to document everything properly.

With the right approach to proactive tax planning, many of the things you are already doing this summer can become part of a smart, compliant tax strategy.

Business Travel Deductions: What Actually Qualifies

The Primary Purpose Test

The IRS uses a "primary purpose" test for business travel. If the primary reason for a trip is business, most of your transportation costs are deductible even if you added a few personal days.

Here is how it generally works:

- Flights and transportation: Fully deductible if the primary purpose is business.

- Hotel stays: Deductible for the business days of the trip.

- Meals: 50% deductible when business is discussed or the meal has a clear business purpose.

- Personal days: Not deductible, but they do not disqualify your legitimate business expenses either.

Example: You fly to Miami for a three day real estate conference and extend the trip for two personal days. The flight and conference related expenses are deductible. The two extra hotel nights are not. Clean, simple, and totally legitimate.

What You Need to Document

The IRS does not accept "I was doing business." You need records. For every trip, keep:

- Who you met with or the conference or event you attended

- What business was conducted

- When the dates of travel occurred

- Where the location was

- Why it was business related

Apps like Expensify or even a simple notes log tied to your calendar work well. The point is to make documentation a habit, not an afterthought.

Real Estate Investor Tax Strategies: The Summer Edition

Property Tours as Business Travel

Real estate investors often have one of the strongest cases for business travel deductions, especially during summer when travel is more accessible and markets are active.

If you are a real estate investor and you travel to:

- Tour investment properties you are considering purchasing

- Meet with local property managers or contractors

- Attend a real estate investor summit or local REIA meeting

- Evaluate a new market for portfolio expansion

Those trips carry legitimate deduction potential. The key, again, is documentation and ensuring business is the primary purpose.

The Real Estate Professional Status Advantage

If you qualify as a Real Estate Professional under IRS rules (750+ hours per year in real estate activities, more than 50% of your working time), summer is a great time to track and audit your hours. This status can unlock the ability to deduct rental losses against ordinary income, a powerful tax lever that most investors never fully leverage.

Cost Segregation: A Powerful Tool That Does Not Require REPS or STR Status

Most investors assume they need Real Estate Professional Status (REPS) or a short term rental loophole to unlock big depreciation benefits. That is not the case.

Cost segregation is an IRS approved strategy that allows real estate investors to accelerate depreciation on specific components of a property, things like flooring, fixtures, landscaping, and personal property. This can generate substantial paper losses that offset your taxable income, often without needing REPS or STR classification at all.

Summer is a great time to explore this strategy, especially if you recently acquired property or are planning a purchase before year end.

Watch this to understand exactly how it works:

Cost Segregation for Real Estate Investors: Maximize Tax Savings Without REPS or STR Loopholes

This is one of the most underutilized strategies in real estate tax planning, and it applies to far more investors than most people realize.

Short Term Rental Strategies

If you own or are evaluating short term rentals (Airbnb, VRBO), summer is peak revenue season but also a planning opportunity. Understanding the tax treatment of short term rentals, especially the 14 day rule, the average rental period, and material participation, can significantly affect how your rental income is taxed.

Meals, Networking Events, and Client Entertainment

The Tax Cuts and Jobs Act (TCJA) eliminated the deduction for entertainment expenses, but business meals are still 50% deductible when:

- The expense is ordinary and necessary for your business

- You or an employee are present

- The meal is not lavish or extravagant

- There is a clear business purpose (document it before or after the meal)

Summer is full of opportunities here: client lunches, networking dinners, team strategy sessions over meals. Each one is a deduction waiting to be captured if documented correctly.

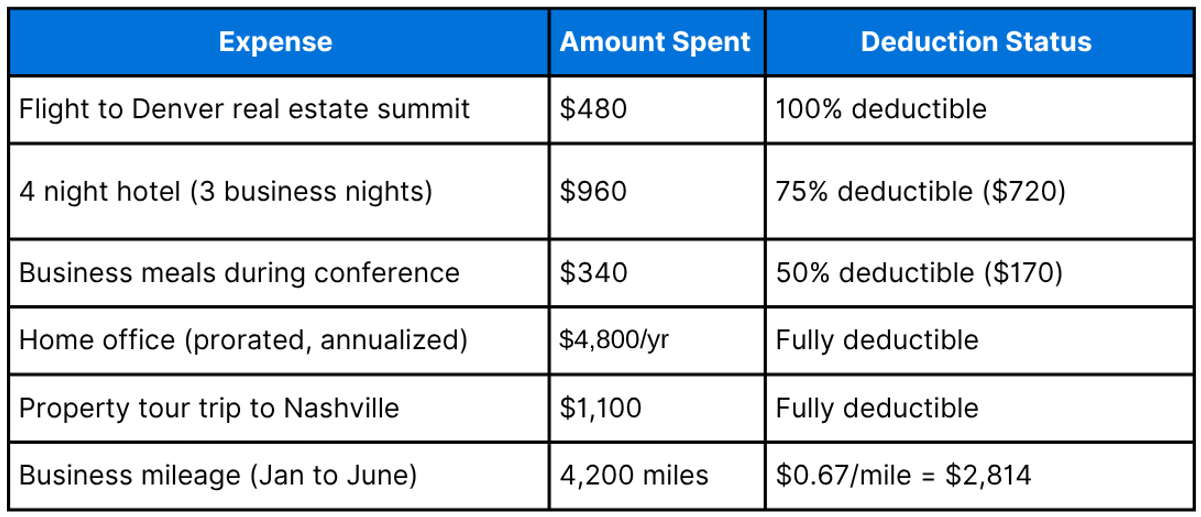

Real Life Tax Planning Example

Meet Sarah: Real Estate Investor and Small Business Owner

Sarah runs a boutique property management company and owns six rental units. In past years, she filed her taxes reactively, handing documents to her accountant in March and hoping for the best.

This year, she worked with a proactive CPA starting in Q2. Here is what changed:

Estimated total deductions added through proactive planning: approximately $10,000+

At a 35% effective tax rate, that is approximately $3,500 in tax savings just from summer activity alone, when combined with other proactive strategies.

And that does not include entity structure optimization, depreciation strategies, or cost segregation. All of these are things a tax planning for business owners specialist would layer in on top of the baseline deductions above.

5 Common Mistakes Business Owners Make With Summer Expenses

1. Treating Personal Trips as Business Trips

The IRS knows the difference. Taking your family to Disney and calling it a "business retreat" is not a strategy, it is a red flag. Mixed purpose travel requires an honest assessment of primary purpose.

2. Skipping Documentation

The deduction is only as good as the paper trail behind it. Verbal recollections and vague credit card statements will not survive an audit. Document in real time, not three months later.

3. Missing the 50% Meal Deduction

Business owners either over claim (deducting entertainment that no longer qualifies) or under claim (forgetting to capture legitimate meal deductions). Both are costly mistakes.

4. Ignoring Mileage

If you are driving to properties, client sites, or networking events, your mileage is deductible. Many business owners either do not track it or do not realize how quickly it adds up. At $0.67 per mile in 2024, 5,000 business miles equals $3,350 in deductions.

5. Waiting Until Q4 or April to Think About Taxes

This is the biggest mistake of all. Tax planning only works when it is proactive. By the time year end arrives, most of the meaningful planning windows have already closed. Summer is the perfect time to get ahead.

Frequently Asked Questions

Q1: Can I deduct a vacation that includes a few business meetings?

Generally, no, not the personal portions. If business is the primary purpose of the trip, your transportation and business day expenses may be deductible. But a vacation with a few calls sprinkled in does not qualify as a business trip.

Q2: What is the best way to document business travel?

Keep a travel log or use an app that captures the date, destination, business purpose, and who you met with. Save all receipts. Tie your calendar entries to your expenses. This creates a strong, audit ready record.

Q3: Can real estate investors deduct travel to look at properties they do not end up buying?

Yes. If you are actively in the business of acquiring and managing real estate, travel to evaluate properties can be deductible even if you do not purchase them. The activity must be part of your business, not a passive curiosity.

Q4: Are home office deductions still available in 2024?

Yes, for self employed individuals and business owners. The home office must be used regularly and exclusively for business. You can use the simplified method ($5 per sq ft, up to 300 sq ft) or the actual expense method, which is more complex but often results in a higher deduction.

Q5: How does the 14 day rule affect my short term rental deductions?

If you rent a property for fewer than 15 days per year, the rental income is tax free but you also cannot deduct rental expenses. If you rent for 15 or more days, different rules apply based on personal use. Understanding this distinction before summer peak season is critical for short term rental owners.

Q6: Should I form an S Corp or LLC before deducting business travel?

Your entity structure affects how deductions flow, but deductions for sole proprietors (Schedule C), S Corps, and LLCs are all available with proper documentation. A proactive CPA can help you determine whether restructuring would enhance your overall tax position.

Q7: What triggers an IRS audit related to travel expenses?

Excessive travel deductions relative to reported income, high meal deductions, and mixed use travel without documentation are common triggers. The solution is not to avoid deductions. It is to claim them correctly and document everything.

Final Thoughts

Summer is not a tax break. It is a tax opportunity.

The business owners who thrive financially are not always the ones who earn the most. They are the ones who keep the most. And keeping more requires a mindset shift: from reactive tax filing to proactive tax planning.

Every business trip, client meal, real estate tour, and networking event this summer is either a tax opportunity or a missed one. The difference comes down to strategy, documentation, and working with the right team.

At INVESTOR FRIENDLY CPA®, we believe your CPA should be as proactive about finding opportunities as you are about building your business.

Next Steps

Here is what you can do right now:

- Audit your summer plans. Identify trips, meals, and events that may have a business purpose and start documenting today.

- Track your mileage. Use MileIQ, TripLog, or a simple spreadsheet. Start now.

- Review your entity structure. If you are a sole proprietor or have grown significantly, now is the time to evaluate whether your current setup still serves you.

- Learn about cost segregation. Watch the video above and explore whether this strategy applies to your portfolio.

- Get ahead of Q4. Mid year is the ideal time to course correct and capture opportunities before the planning window closes.

Be the First to Experience a Smarter Way to Plan Your Taxes

Stop filing taxes. Start planning them.

At INVESTOR FRIENDLY CPA®, we work exclusively with business owners, entrepreneurs, and real estate investors who are serious about building wealth and keeping it.

TaxMD™ is our upcoming proactive tax planning software built specifically for investors and entrepreneurs like you. It is designed to help you identify what you are overpaying, capture strategies you are missing, and put a real tax plan in place year round, not just in April.

TaxMD™ is not live yet, but it is coming soon. And when it launches, the business owners on the waitlist will be the first to access every strategy covered in this post and more. Join the TaxMD™ Waitlist today and be the first to experience proactive tax planning built for the way you actually do business.

In the meantime, schedule a FREE tax strategy consultation with INVESTOR FRIENDLY CPA® and let us show you exactly where your biggest opportunities are hiding this summer.

Because the best time to plan your taxes was yesterday. The second best time is today.

- Summer travel, meals, and real estate trips can be legitimate tax deductions if documented properly.

- Proactive tax planning during the summer months can position you for significant savings by year end.

- The IRS has clear rules around business travel and mixed purpose trips. Knowing them protects you.

- Real estate investors have unique summer opportunities to combine property tours with deductible expenses.

- Working with a proactive CPA before Q4 means fewer surprises and more money kept in your pocket.

.png)

.png)

.png)